2024 guide to payment gateway integration

Seamless and secure payment processing is crucial for any app involving financial transactions.

Whether you’re building an e-commerce platform, a peer-to-peer payment app, or a subscription service, you need a reliable solution to accept payments.

This guide explains payment integration for business owners. It covers the payment process and how to add it to your app or website. You’ll learn to choose and implement the best payment method for your business.

Payment process

Let’s start by discussing the payment process from both the customer’s perspective and the technical point of view.

Customer’s point of view

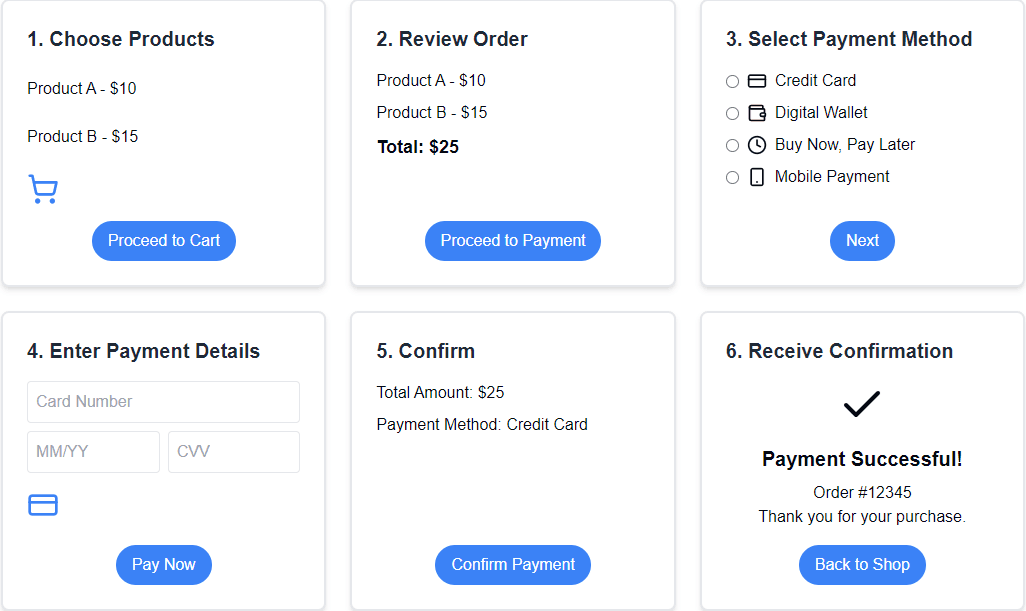

Here’s an example of a basic e-commerce transaction. On the customer side it looks like this:

- Add the desired items to your cart.

- Check the order details (items, prices, shipping costs).

- Choose your preferred payment method (card, bank transfer, etc.).

- Fill in the required information (e.g., card number).

- Approve the transaction.

- A confirmation message will be displayed on the screen and/or sent to your email.

Technical point of view

The process is simple and obvious from a user’s perspective. However, there’s an array of steps that take place underneath:

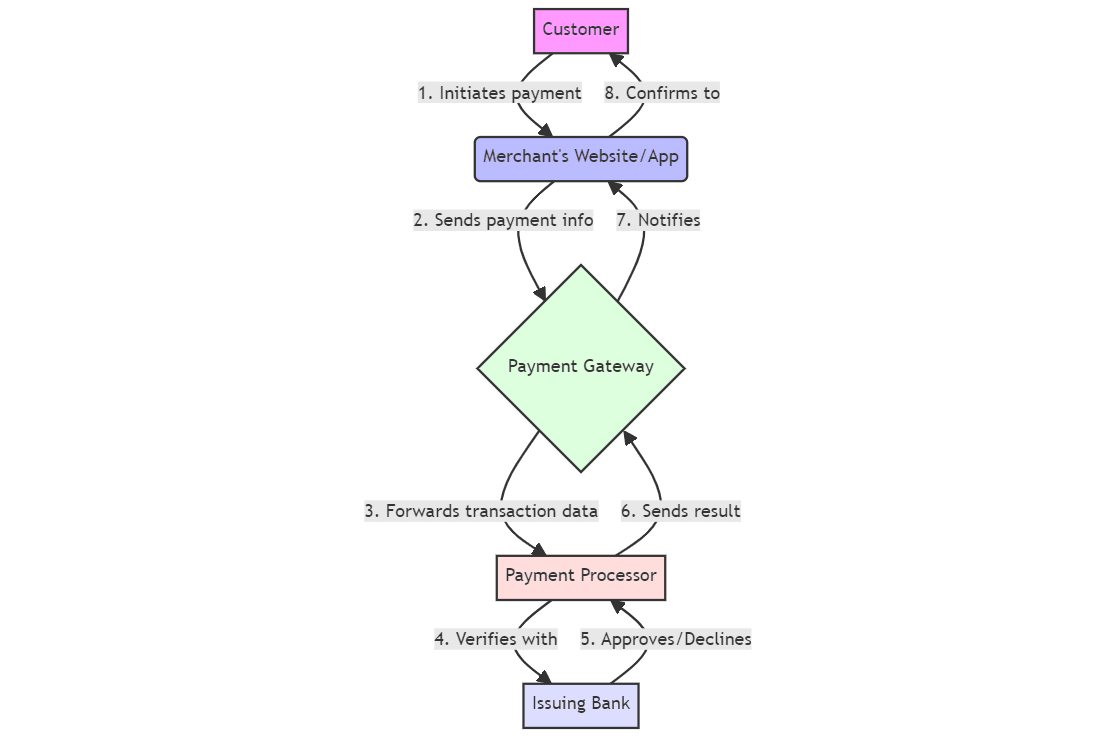

On the tech side, a basic payment process typically flows like this:

- The customer initiates a payment in your app.

- Your app sends the payment information to the payment gateway.

- The payment gateway forwards the transaction details to the payment processor.

- The payment processor communicates with the customer’s bank (issuing bank) to verify the payment.

- The issuing bank approves or declines the transaction.

- The payment processor sends the result back through the chain: to the payment gateway, then to your app.

- Your app confirms the payment status to the customer.

Throughout this process:

- The payment gateway acts as the secure entry point for the transaction, and the payment processor handles the actual movement of funds between financial institutions. It’s also worth mentioning that in some cases, the payment gateway and payment processor may be the same entity or closely integrated.

- After authorization, the funds are typically settled (transferred) between banks a few days later.

If we combine the process from both customers and technical (back-office) perspectives, that’s what it would look like:

In general, that’s what the process is all about. Let’s discuss in more detail the technical components that make it possible.

Key component of payment integration

In this part, we’ll examine the elements that enable digital payments and discuss their role in the payment process.

Your app

Your (web or mobile) app is the foundation of the payment integration process. It serves as the interface where customers interact and make payments.

Key functions include:

- Providing the user interface for initiating transactions

- Collecting and securely transmits payment information

- Integrating with payment gateways or providers

- Communicating transaction status to users

Payment gateway

A payment gateway is the front-line service that initiates the payment process. When a customer makes a purchase, the payment gateway receives the payment information from a website or app. It then securely passes this information along to the next step in the process (payment processor).

Types:

- Hosted: Customers directed to a separate payment page.

- Self-hosted: Payment handled on your app’s server.

- API-based: Combination of both.

- Local bank integration.

Core functions:

- Encrypt sensitive payment data

- Route transaction information to the appropriate processors

- Request and relay payment authorizations

Payment gateway provider examples: Stripe, Authorize.Net, PayPal, Braintree

Payment processor

A payment processor handles the actual transfer of funds between banks during a transaction.

Examples: First Data (now part of Fiserv), TSYS (Total System Services, now part of Global Payments), Worldpay (now part of FIS)

At this point, you know the technicalities, and are probably asking yourself: “Okay, so what do I do now? How do I actually implement a payment system in my product?” Let us answer.

Custom payment gateway integration services

Our team specializes in payment gateway integration and custom solutions tailored to your unique business needs across various industries, with a special focus on fintech & blockchain, digital health, and e-commerce.

Whether you’re looking to add new secure payment methods to your or create a smoother checkout process, we’ve got you covered.

Contact our experts now to get started on your custom payment solution >>

How to integrate a payment gateway into a website or app?

Here’s a step-by-step guide to help you move from understanding the technicalities to actually implementing a payment system.

Step 1: Define your payment requirements

Understand your business model

Determine what type of transactions you need to process.

Understanding your business model is crucial when implementing a payment system because it directly influences the design and functionality of the payment system you choose: the types of transactions you will handle, the volume of payments, the preferred payment methods of your customers, and the regulatory requirements you must adhere to.

What’s more, each type of business model comes with its own challenges: an e-commerce business with global customers will need a payment system that supports multiple currencies and international payment methods, and a subscription-based service may prioritize recurring billing features. If you’re still figuring out the best way to monetize your app, exploring different monetization strategies can help shape your payment integration.

- We’ve discussed e-commerce, subscription services, and P2P payments challenges at the end of the article, so feel free to rush over to this section: Payment integration challenges & insights for different business models

Identify payment methods

Identify the geographical regions you will operate in and the payment methods popular in those regions. Based on that, decide on the payment methods you want to offer (e.g., credit/debit cards, digital wallets, bank transfers, mobile payments, cryptocurrency).

Recognizing the payment methods directly impacts the convenience and accessibility of your service for customers, which can significantly influence their purchasing decisions. Different regions have varying preferences and levels of trust in certain payment methods.

For example, credit and debit cards were the most used digital payment in Canada in 2023; in the UK – e-wallets. On the other hand, local payment methods reigned in the Netherlands (more than half of all e-commerce payment transactions were done with iDEAL, a domestic bank transfer system) or Poland, where paying with 6-digit BLIK codes is the most popular online payment method.

- Cards are widely accepted, offering immediate payment confirmation, but also come with a high dispute rate. Example: Visa

- Digital wallets provide convenience and an added layer of security through customer verification. Example: PayPal

- Bank debits involve direct fund pulls from the customer’s account, offering the lowest dispute rate and suitability for recurring payments. Example: ACH

- Bank redirects are authenticated bank debits with immediate confirmation, though typically not supporting recurring payments. Example: iDEAL

- Bank transfers are customer-initiated fund pushes, ideal for large transactions but with delayed confirmation and no dispute mechanism. Example: SWIFT

- Buy Now, Pay Later (BNPL) options offer customers immediate financing, potentially boosting conversion rates, but without support for recurring payments. Example: Klarna

- Cash-based vouchers are physical payment methods, often used in markets with low card penetration, but with delayed confirmation and no dispute options. Example: Boleto

- Real-time payments enable near-instant transfers, combining the speed of cards with the lower costs of traditional bank transfers. Example: Faster Payments

Step 2: Choose a payment provider

While a payment provider is not a distinct element in the payment processes, it plays a key role in enabling them.

What is a payment provider?

A payment service provider (PSP) is a third-party company that helps businesses accept online payments. PSPs act as a bridge between businesses and banks, and handle most of the parts of processing payments, offering:

- Payment gateway

- Payment processing

- Fraud detection and prevention

- Compliance and security

- Currency conversion

- Reporting and analytics

- Customer support

Some well-known PSPs include PayPal, Stripe, and Square.

Using a PSP can save time and money, because businesses don’t need to build their own payment systems or deal directly with banks. PSPs also handle many complex rules and regulations about handling money.

In exchange, they usually charge a small fee for each transaction they process. Some might also have monthly fees or charges for extra services.

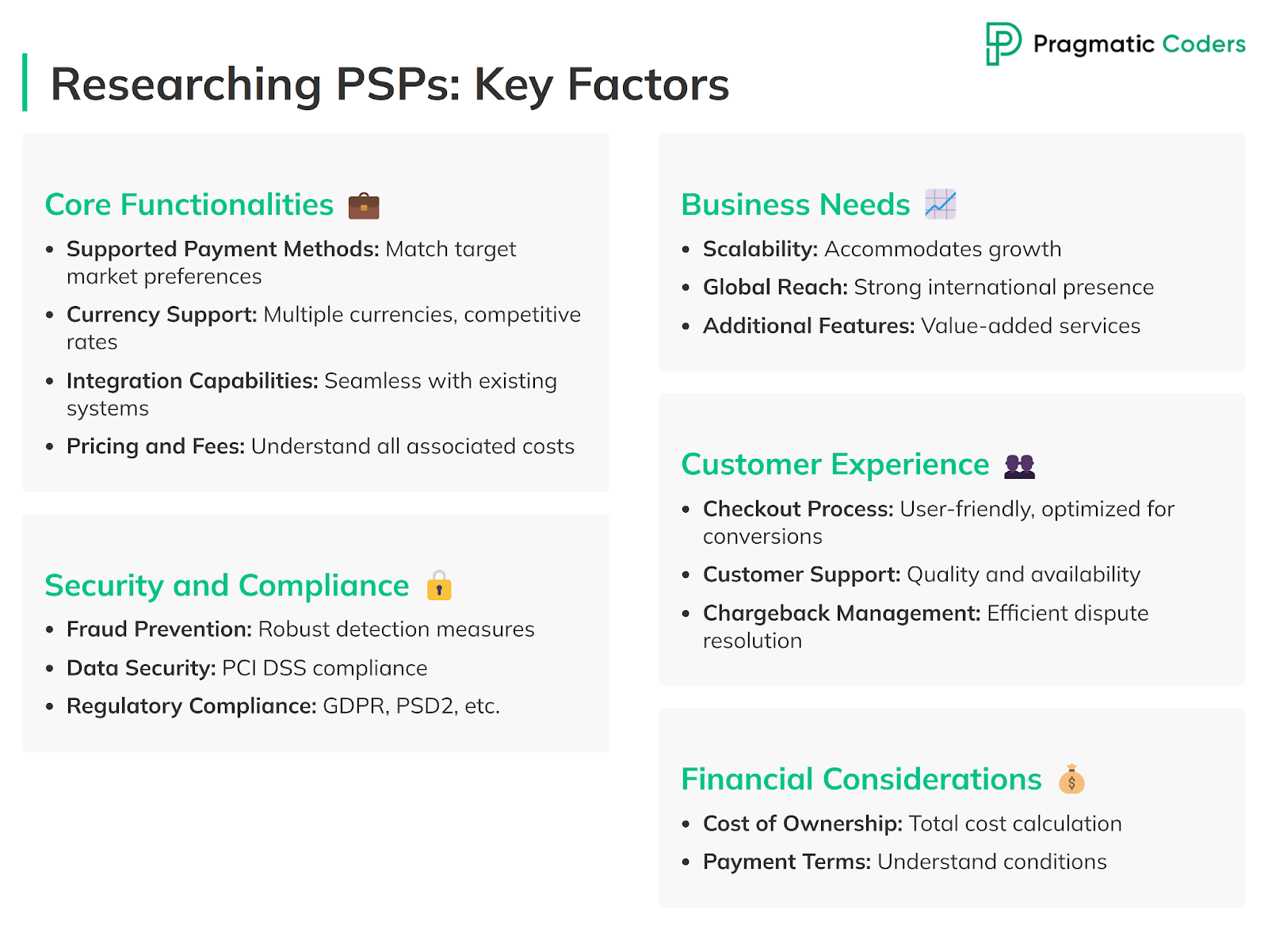

Research payment service providers: Key factors to consider

When choosing a payment service provider (PSP), it’s important to consider several key areas.

Let’s explore these in detail to help you make an informed decision.

Core functionalities

Core functionalities are the backbone of any PSP.

Look for a provider that supports the payment methods your customers prefer, whether that’s credit cards, digital wallets, or bank transfers. If you sell internationally, make sure the PSP can handle multiple currencies and offers fair exchange rates.

It’s also crucial to check how well the PSP integrates with your current systems. You don’t want a payment solution that causes technical headaches.

Lastly, take a close look at the pricing structure. Understand all the fees involved, from transaction costs to monthly charges, so you can budget accurately.

Security and compliance

Security and compliance should be top priorities when selecting a PSP. Your customers trust you with their financial information, so choose a provider with strong fraud prevention measures.

Look for PSPs that follow strict data protection rules, like PCI DSS compliance. These standards help keep sensitive information safe.

Also, make sure the PSP follows relevant laws and regulations, especially if you operate in different countries. This can save you from legal troubles down the road.

CX

The customer experience can make or break your online sales.

A good PSP offers a smooth, user-friendly checkout process. This means fewer abandoned carts and happier customers. Consider the quality of customer support the PSP provides. If something goes wrong, you want to be able to get help quickly.

Look into how the PSP handles disputes and chargebacks. A provider with a fair, efficient process can save you time and money when dealing with customer issues.

Business needs

Your business needs should guide your choice of PSP.

Think about your growth plans. Can the PSP handle more transactions as your business expands?

If you want to sell in other countries, look for a provider with a strong global presence. Some PSPs offer extra features that might be useful, like tools for managing subscriptions or analyzing your sales data. These extras can add value to your business beyond just processing payments.

Finance

Financial considerations are crucial when choosing a PSP.

Calculate the total cost of using the service, including all fees and potential integration expenses.

Understand the payment terms – how quickly will you receive your money after a sale?

Some PSPs like Adyen might require you to keep a reserve balance, which can affect your cash flow. Make sure you’re comfortable with all the financial aspects before making your final decision.

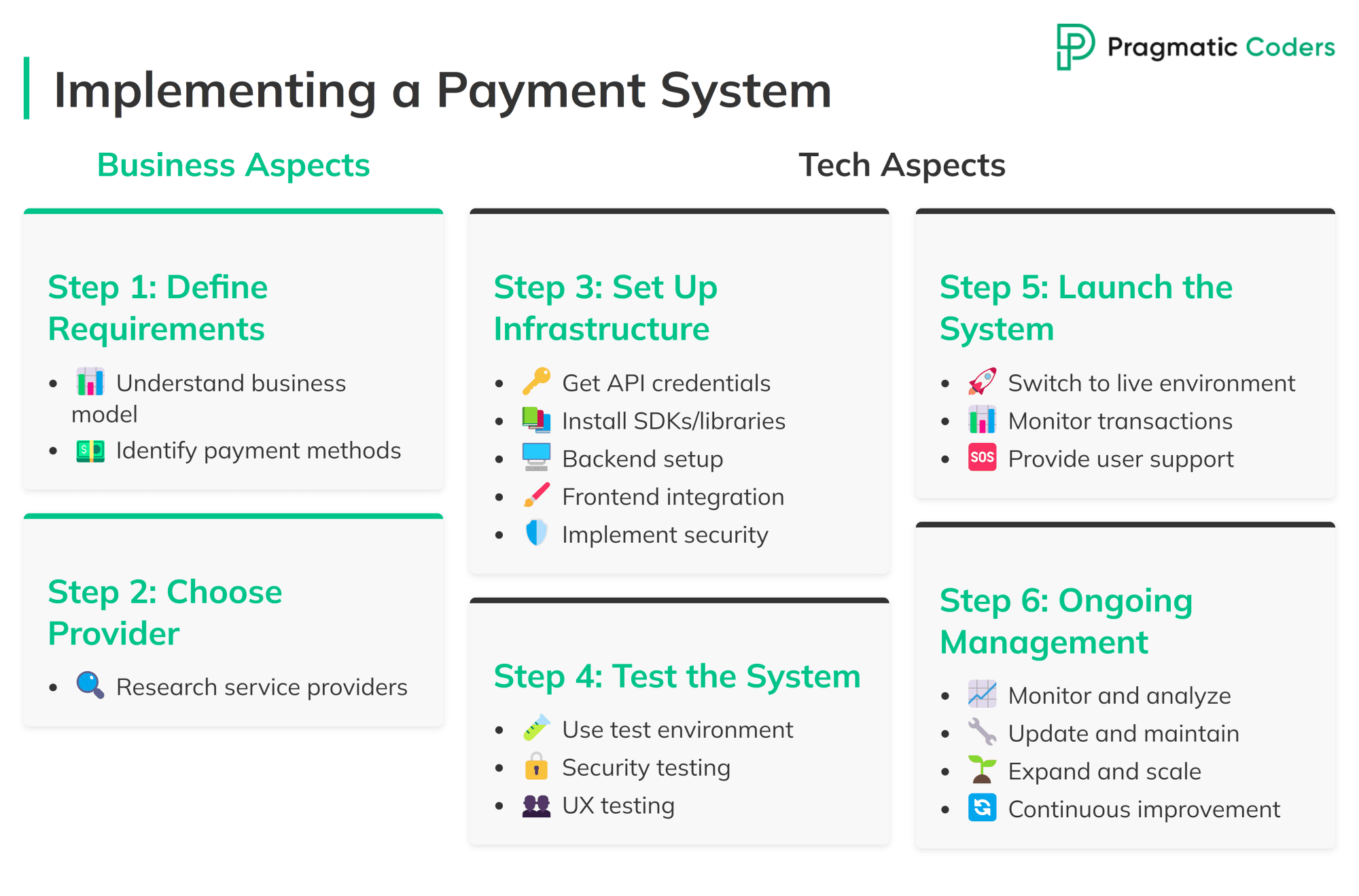

Step 3: Set up the technical infrastructure

- Sign up and get API credentials:

- Register with the chosen payment provider and obtain your API keys (both test and live environments).

- Install SDKs or libraries:

- Install the relevant SDKs or libraries provided by the payment provider for your platform (e.g., web, iOS, Android).

- Backend setup:

- Set up your backend to handle payment requests, create payment sessions, and store transaction data securely.

- Implement webhooks to receive real-time updates from the payment provider (e.g., payment success, failure, refunds).

- Frontend integration:

- Integrate the payment forms or payment gateway UI into your product.

- Ensure that the user experience is smooth, intuitive, and secure (e.g., using hosted payment pages or custom forms).

- Implement security measures:

- Ensure all data transmitted is encrypted (use HTTPS).

- Implement tokenization to protect sensitive payment information.

- Use strong authentication methods (e.g., MFA) for admin access to payment settings.

Step 4: Test the payment system

- Use test environment:

- Test the integration using the sandbox environment provided by your payment provider.

- Simulate various payment scenarios (e.g., successful payment, declined transaction, refunds, chargebacks).

- Conduct security testing:

- Perform security audits and penetration testing to ensure your payment system is secure.

- Test for vulnerabilities like SQL injection, XSS, and CSRF.

- User experience testing:

- Ensure the payment flow is smooth and intuitive.

- Check for responsiveness on different devices and browsers.

Step 5: Launch the payment system

- Switch to live environment:

- Once testing is complete and successful, switch to the live environment by using your live API credentials.

- Monitor transactions:

- Monitor the first few transactions closely to ensure everything works as expected.

- Set up alerts for any anomalies or failed transactions.

- Provide user support:

- Set up customer support channels to assist users with payment-related issues.

- Offer clear instructions and FAQs on how to use the payment system.

Step 6: Ongoing management and optimization

- Monitor and analyze:

- Regularly monitor transaction reports, conversion rates, and payment failures.

- Use analytics to identify areas for improvement (e.g., optimizing checkout flow, reducing cart abandonment).

- Update and maintain:

- Keep the payment integration up-to-date with the latest security patches and provider updates.

- Regularly review your compliance with PCI DSS and other relevant regulations.

- Expand and scale:

- As your business grows, consider adding more payment methods, expanding to new regions, or integrating additional features like subscriptions or loyalty programs.

- Continuous improvement:

- Gather feedback from users on the payment experience and make iterative improvements.

- Stay informed about new payment technologies and finance trends to keep your system future-proof.

Payment integration challenges & insights for different business models

Payment integration is a crucial aspect of modern business models, especially for P2P, e-commerce, and subscription services.

While each model has unique needs, they all share the goal of making transactions smooth and secure.

Let’s explore how these different business types handle payments.

P2P platforms

Starting with P2P (peer-to-peer) platforms, we see a focus on speed and simplicity.

Apps like Venmo and Cash App thrive on quick, easy transfers between users. To achieve this, they often link directly to bank accounts or debit cards, cutting out middlemen and reducing fees.

However, with great speed comes great responsibility – security is paramount in P2P payments. As a result, these apps employ strong encryption and often require two-factor authentication (2FA) to keep users’ money safe.

Moreover, P2P services are evolving beyond simple money transfers.

Many now incorporate social features, allowing users to share emojis or messages with their payments. This adds a fun, engaging element to what could otherwise be a dull transaction.

Additionally, some P2P platforms are branching out into new territories, such as cryptocurrency trading or investment options, to stay competitive in a crowded market.

E-commerce

Shifting gears to e-commerce, we find a different set of challenges and solutions.

Online stores must cater to a wide range of customer preferences, which means offering multiple payment methods. From credit cards and PayPal to newer options like Apple Pay, the more choices available, the better chance of making a sale.

One of the biggest hurdles in e-commerce is cart abandonment – when customers leave without completing their purchase. To combat this, many sites have implemented one-click purchasing or guest checkout options. These streamlined processes aim to convert more browsers into buyers by reducing friction at the crucial moment of purchase.

Just like their P2P counterparts, e-commerce platforms also prioritize security. Many use advanced fraud detection systems to spot suspicious activity, protecting both the business and its customers. For stores selling internationally, there’s the added complexity of handling different currencies and complying with various tax laws.

Subscription

Lastly, we come to subscription businesses, which face their own unique set of payment challenges.

The backbone of these services is the recurring billing system, which automatically charges customers on a set schedule. However, this seemingly simple process can be fraught with complications.

Failed payments, for instance, are a common issue that can lead to involuntary churn – losing customers not because they want to leave, but due to payment problems. To mitigate this, good subscription platforms implement systems to retry failed payments and notify customers, giving them a chance to update their information before losing access.

Flexibility is another key feature of successful subscription models.

Many offer easy options to upgrade, downgrade, or pause subscriptions, keeping customers happy and reducing voluntary churn. Free trials are also common, requiring a payment system that can smoothly transition users from free to paid plans without causing friction.

Furthermore, as subscription services evolve, many now offer multiple tiers – perhaps including basic, premium, and family plans. This complexity requires a robust payment system capable of handling various pricing structures and billing cycles.

Across all these business models, one common thread emerges: the growing importance of mobile optimization of fintech apps. With more people managing their finances, shopping, and subscribing to services via smartphones, a seamless mobile payment experience has become essential for success.

- Payment gateway integration is just one part of a much larger puzzle. To explore the broader challenges of software integration and how to tackle them effectively, check out our guide: Beyond Just ‘Integrate It’.”

Conclusions

Payment integration is a crucial aspect of modern business, whether you’re running a P2P platform, an e-commerce store, or a subscription service.

Each model has its unique challenges, but they all share the need for secure, efficient, and user-friendly payment systems with a decent technological backbone.

Don’t let the complexities hold you back. Contact us today, and we’ll help you implement a robust, tailored payment solution that meets your specific business needs.