How to Start a Fintech Company? Fintech Startup Building Guide

The fintech landscape is evolving at an unprecedented pace, reshaping how we interact with money and financial services. As we move towards 2025, the convergence of cutting-edge technologies, changing consumer expectations, and a global push for financial inclusion is creating an unprecedented opportunity. Innovators now have a unique chance to make their mark in the fintech space.

Several factors make the upcoming year ideal for launching a fintech venture:

- Accelerated digital transformation post-pandemic: Over 40% of adults in low- and middle-income economies made their first digital payment during the pandemic.

- Regulatory support through “sandboxes” in many countries: There are over 70 regulatory sandboxes worldwide.

- Maturation and expansion of AI: The global AI market is expected to reach $370.22 billion by 2025.

- Rising demand for financial inclusion: Nearly 13 million adults in the UK alone feel excluded from the financial system, facing significant barriers to accessing affordable credit.

- Rapid market growth: The global fintech market is projected to reach $460 billion by 2025.

This comprehensive guide will walk you through every crucial step of starting a fintech startup. By the end, you’ll have a clear roadmap to turn your fintech vision into reality.

Key Steps to Start a Fintech Company

|

Understanding the Fintech Market

Before diving into the process of starting your fintech company, it’s crucial to understand the ecosystem you’ll be operating in. This knowledge will help you identify opportunities, navigate challenges, and position your startup for success.

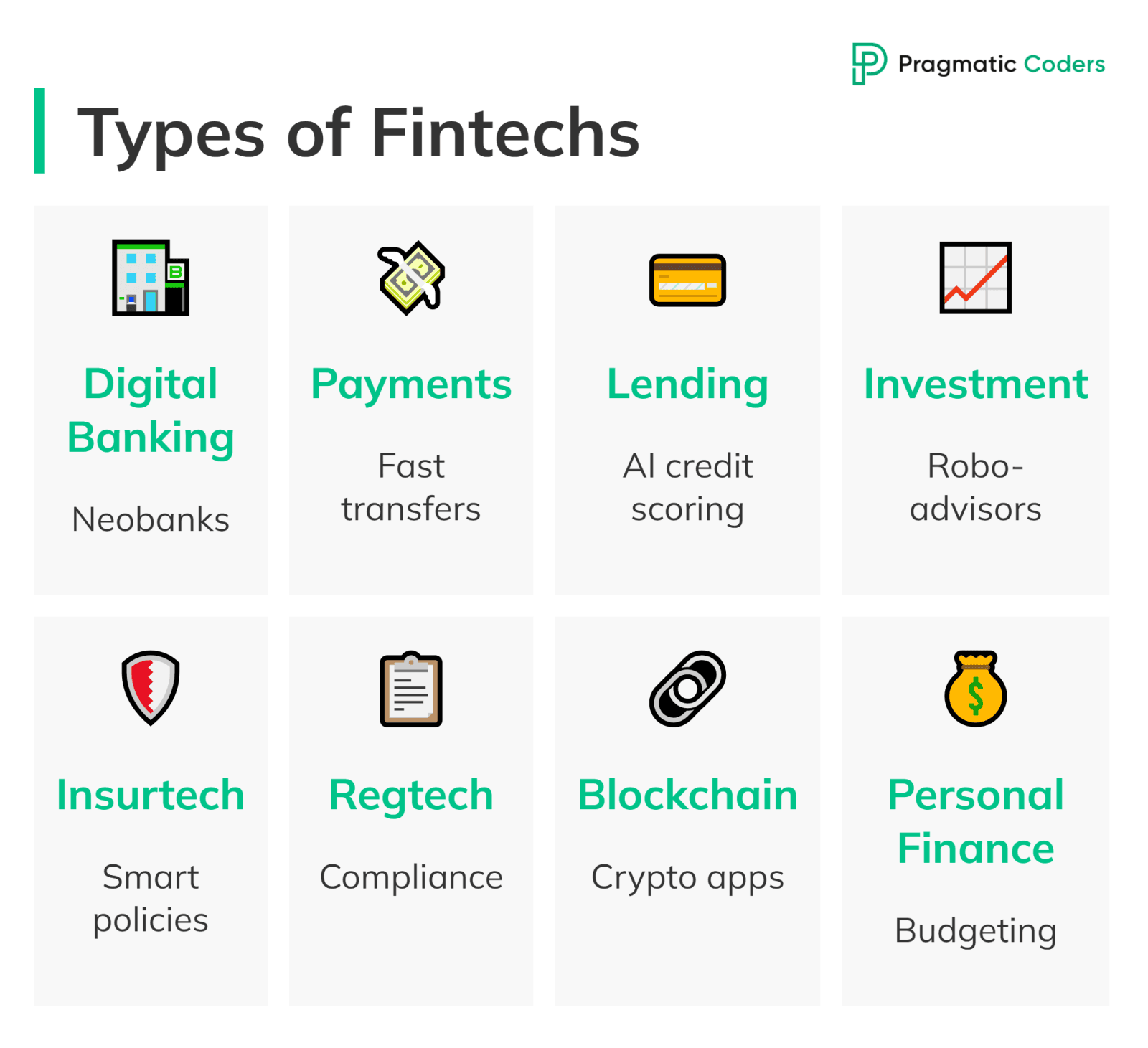

Types of Fintech Businesses

Fintech, short for financial technology, refers to the use of technology to improve and automate financial services. Fintech companies can be broadly categorized into several types:

- Digital Banking: Neobanks and challenger banks offering fully digital banking services

- Payments and Remittances: Companies facilitating fast, low-cost money transfers and payments

- Lending and Credit: Platforms offering alternative lending solutions, often using AI for credit scoring

- Investment and Wealth Management: Robo-advisors and digital investment platforms

- Insurtech: Technology-driven insurance solutions

- Regtech: Companies helping financial institutions comply with regulations

- Blockchain and Cryptocurrency: Platforms leveraging blockchain for various financial applications

- Personal Finance Management: Apps helping individuals budget, save, and manage their finances

Current Fintech Market Trends and Opportunities

As we move toward 2025, several trends are shaping the fintech landscape:

- Embedded Finance: The integration of financial services into non-financial products and platforms

- AI and Machine Learning: Advanced algorithms improving everything from fraud detection to personalized financial advice

- Open Banking: APIs allowing third-party developers to build applications and services around financial institutions

- Sustainable Finance: Growing focus on ESG (Environmental, Social, and Governance) factors in financial products

- Central Bank Digital Currencies (CBDCs): National governments exploring the development of digital currencies to enhance the efficiency and security of financial systems.

These trends are creating opportunities for innovative startups to disrupt traditional financial services and create new markets.

Regulatory Landscape and Compliance

The regulatory environment for fintech companies is complex and varies significantly by region. However, some common themes include:

- Data Protection: Regulations like GDPR in Europe and CCPA in California set strict rules for handling personal data

- Anti-Money Laundering (AML) and Know Your Customer (KYC): Fintech companies must implement robust processes to prevent financial crimes

- Consumer Protection: Regulations aim to ensure fair treatment of consumers and transparent pricing

- Cybersecurity: Strict requirements for protecting sensitive financial information from cyber threats

- Open Banking Regulations: In many regions, banks are required to share customer data with authorized third parties, creating opportunities for fintech innovators

Navigating the regulatory landscape is crucial for any fintech startup. Engaging legal experts early ensures compliance from day one. Additionally, leveraging regulatory technology (regtech) can streamline this process.

Understanding these fundamental aspects of the fintech ecosystem will provide a solid foundation as you begin your journey to start a fintech company. In the next sections, we’ll delve into the practical steps of turning your fintech idea into a thriving business.

Ideation and Market Research

Starting a successful fintech company begins with a solid idea and thorough market research. This phase is crucial for validating your concept and ensuring there’s a real market need for your solution.

If you’re looking for a good place to start, try out our free AI market research tool!

Identifying Pain Points in Financial Services

The most successful fintech companies solve real problems. Begin by identifying pain points in existing financial services:

- High fees or hidden charges

- Slow transaction processing times

- Poor user experience in traditional banking apps

- Limited access to credit for certain populations

- Lack of personalized financial advice

Conduct surveys, interviews, and focus groups with potential customers to understand their frustrations with current financial services. Look for patterns and recurring issues that could be addressed with innovative fintech services.

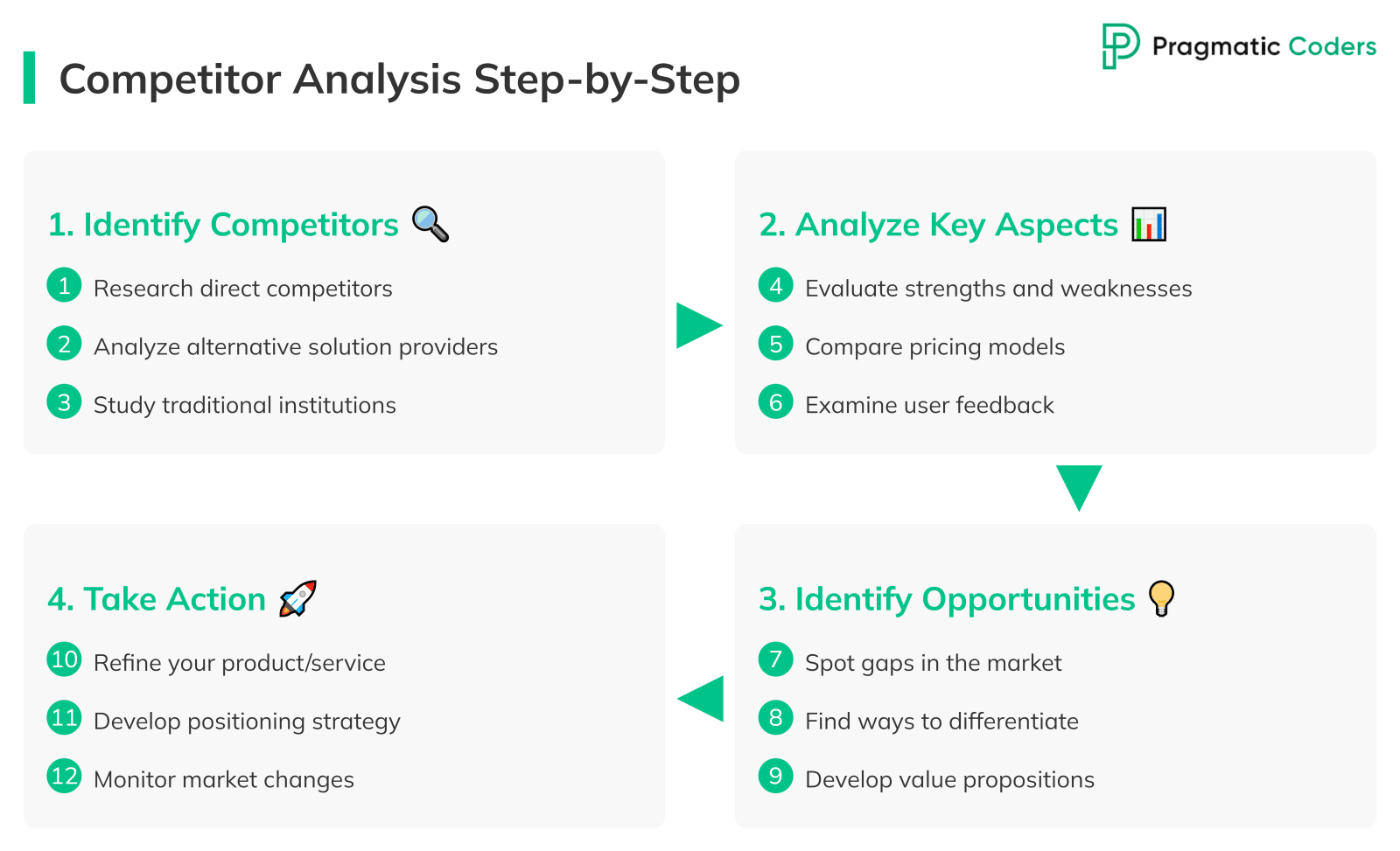

Conducting Thorough Competitor Analysis

Once you’ve identified a potential problem to solve, research existing solutions:

- Analyze direct competitors offering similar services

- Investigate indirect competitors that solve the same problem differently

- Study traditional financial institutions’ offerings in your chosen niche

Look at their strengths, weaknesses, pricing models, and user feedback. This analysis will help you identify gaps in the market and opportunities to differentiate your offering.

Also, here’s a detailed guide to competitor analysis.

Defining Your Unique Value Proposition

Based on your research, define what makes your fintech idea unique:

- Are you offering a more user-friendly interface?

- Can you provide the service at a lower cost?

- Are you targeting an underserved market segment?

- Does your solution leverage new technology in an innovative way?

Your unique value proposition should clearly articulate why customers would choose your service over existing alternatives.

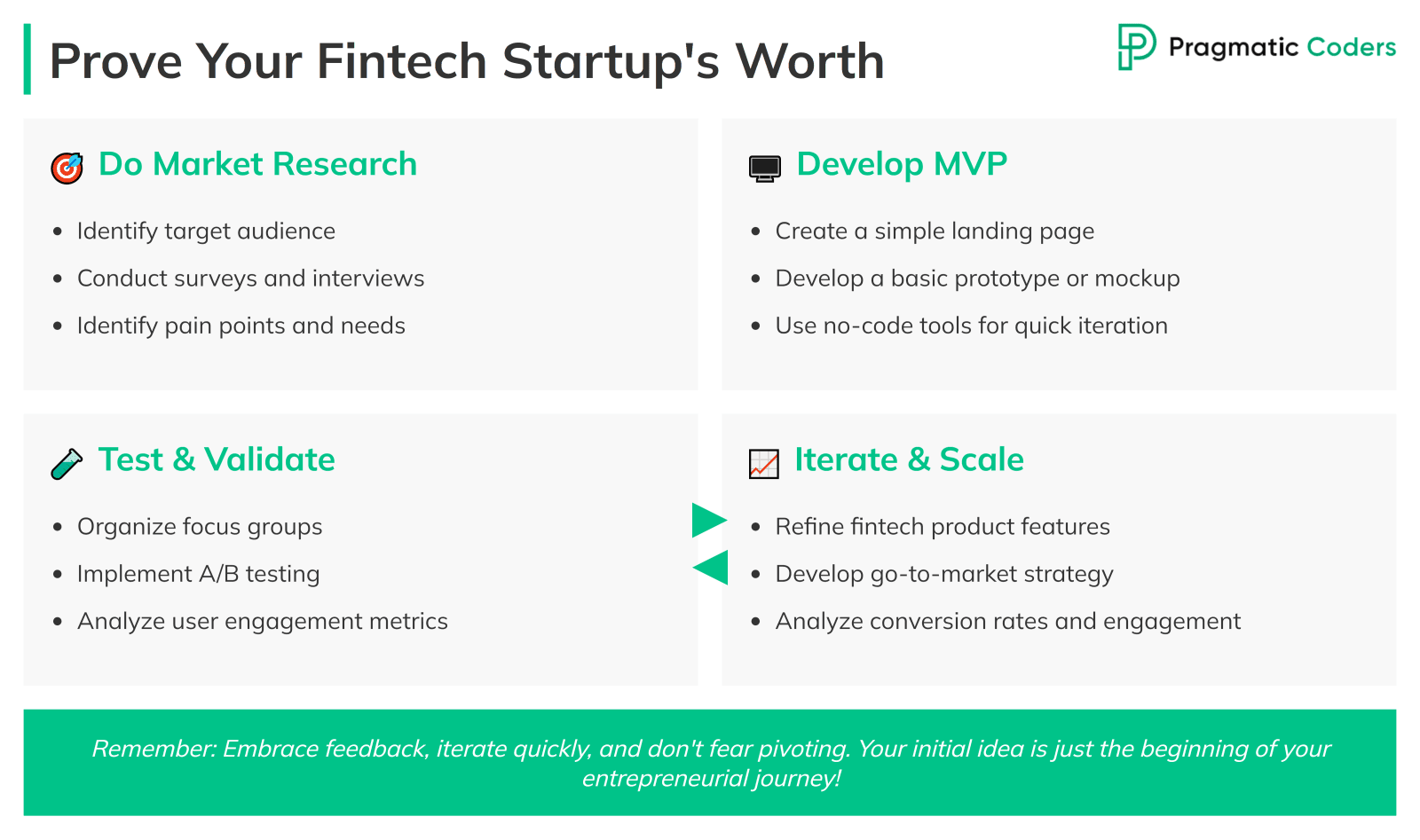

Validating Your Idea with Potential Customers

Before investing significant resources, validate your product idea:

- Create a simple landing page describing your proposed solution

- Develop a basic prototype or mockup of your app

- Present your concept to potential users and gather feedback

- Run small-scale pilot tests if possible

Be prepared to iterate on your idea based on this feedback. Remember, it’s better to discover flaws in your concept early, before you’ve invested heavily in development.

Building Your Fintech Foundation

With a validated idea in hand, it’s time to lay the groundwork for your fintech company.

Choosing Your Niche and Target Audience

While it might be tempting to target a broad market, focusing on a specific niche can be more effective for a startup:

- Clearly define your target audience (e.g., millennials, small business owners, gig economy workers)

- Understand their specific needs and pain points

- Tailor your solution to address these specific challenges

A focused approach allows you to build a strong reputation in one area before expanding.

Developing a Robust Business Model

Your business model should outline how your new fintech company will create value and generate revenue:

- Revenue streams (e.g., transaction fees, subscription model, data monetization)

- Cost structure (fixed costs, variable costs)

- Key resources and activities

- Customer relationships and channels

Consider using tools like the Business Model Canvas to visualize and refine your business model.

Creating a Minimum Viable Product (MVP)

An MVP is a version of your product with just enough features to satisfy early customers and provide feedback for future development:

- Identify the core features that solve your target audience’s main pain point

- Develop a basic version of your fintech software focusing on these core features

- Ensure your MVP adheres to necessary regulatory requirements

- Plan for scalability from the start, even if you’re starting small

Your MVP should be functional enough to provide value and gather meaningful user feedback, but simple enough to develop quickly and cost-effectively.

How long does building an MVP take, and how much will it cost? Look no further than this guide to building an MVP in 2024 for the answer.

Securing Intellectual Property Rights

Protect your fintech innovation:

- File for patents if you’ve developed novel technology

- Register trademarks for your company name and logo

- Use non-disclosure agreements (NDAs) when discussing your idea with potential partners or investors

- Consider the implications of open-source software in your tech stack

- Consult with an intellectual property lawyer to ensure you’re adequately protecting your innovations.

By thoroughly addressing these foundational elements, you’ll be well-positioned to move forward with building and launching your fintech company. In the next sections, we’ll discuss how to assemble the right team and navigate the complex world of fintech development and regulation.

Assembling Your Dream Team

The success of your fintech firm largely depends on the team you build. In this highly specialized field, you need a mix of financial expertise, technological prowess, and entrepreneurial spirit. Fintech app development is no easy feat! For more insights, check out this fintech software development guide.

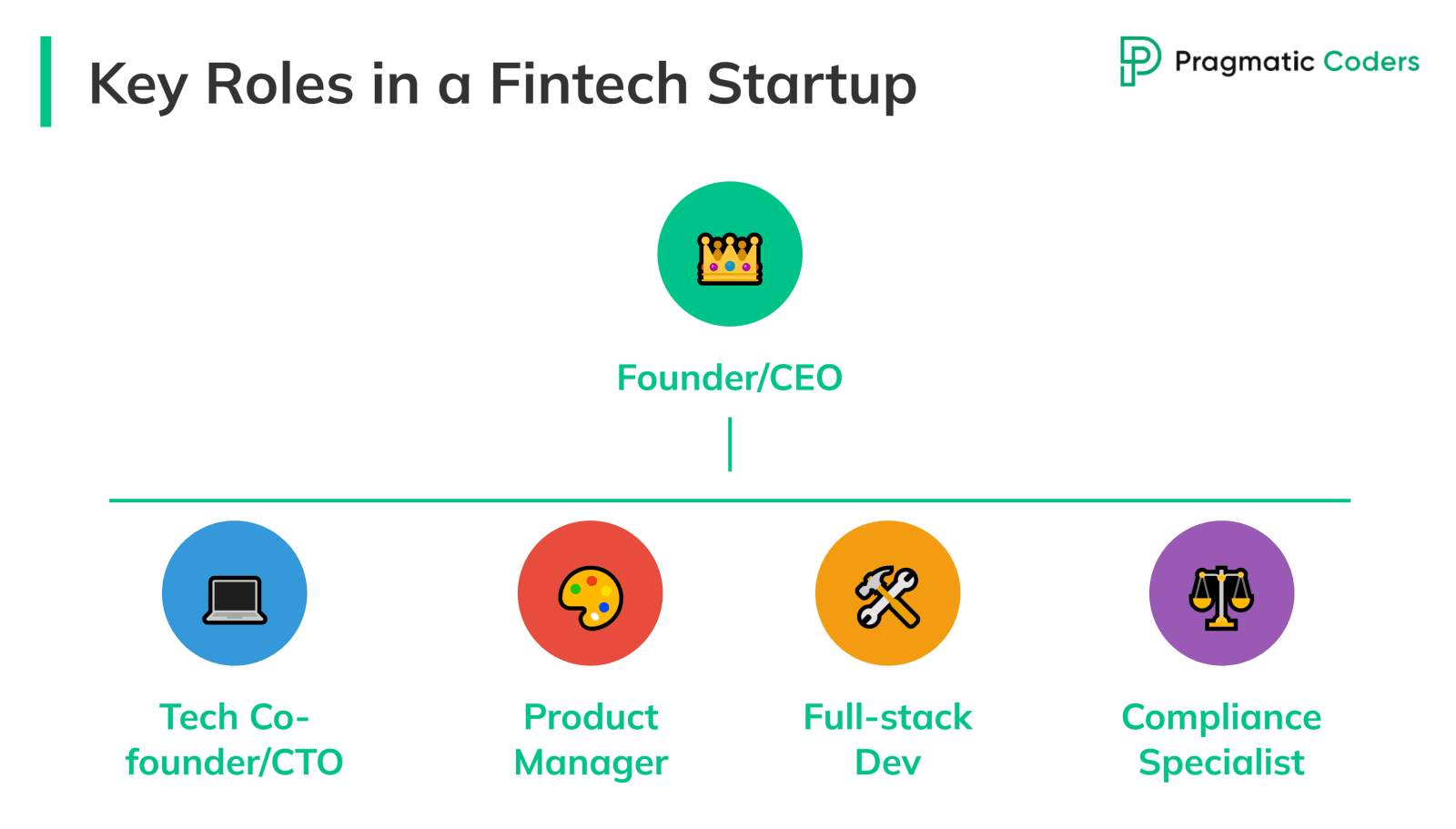

Key Roles to Fill in a Fintech Startup

When you’re just starting out, you need to be lean and efficient. Here are the crucial roles to focus on initially:

- Founder/CEO: This is likely you. You’ll be wearing multiple hats, driving the vision, making key decisions, and often acting as the face of the company.

- Technical Co-founder or CTO: If you’re not technical yourself, this role is crucial. They’ll be responsible for building your MVP, making key technology decisions, and often coding themselves in the early stages.

- Product Manager/Designer: This role is vital for translating your vision into a user-friendly product. They’ll work on user experience, interface design, and feature prioritization.

- Full-stack Developer: In addition to your technical co-founder, you’ll likely need at least one more developer to help build your product quickly.

- Compliance Specialist: Given the regulatory nature of fintech, having someone who understands the compliance landscape is crucial. This could be a part-time role or a consultant initially.

Remember, in the early stages, everyone should be prepared to wear multiple hats. Your product manager might also handle marketing, or your CTO might double as your data scientist. The key is to cover the essential functions – product development, technology, and regulatory compliance – with a small, agile team.

As you grow and secure funding, you can then look to expand your team with specialized roles like dedicated CFO, CCO, data scientists, and additional developers. But in the beginning, focus on the core team that can get your product to market and start gaining traction. Later on, you might want to consider fintech software outsourcing to optimize costs.

Finding the Right Balance of Finance and Tech Expertise

In fintech, it’s crucial to have team members who understand both finance and technology. Look for:

- Finance professionals with a keen interest in technology

- Tech experts who have experience in or enthusiasm for financial services

- Team members who can bridge the gap between these two worlds

Consider partnering with fintech-focused software development agencies or attending industry events to find suitable development partners.

Building a Culture of Innovation and Compliance

Fintech startups need to balance innovation with strict regulatory compliance:

- Foster a culture that encourages creative problem-solving

- Implement robust compliance training for all team members

- Create clear channels for reporting potential compliance issues

- Regularly review and update your compliance policies

Leveraging Advisors and Mentors

Seek guidance from experienced professionals:

- Form an advisory board with fintech industry veterans

- Connect with mentors who have successfully scaled startups

- Join fintech accelerators or incubators for access to resources and networks

Remember, the right advisors can provide invaluable insights, open doors to partnerships, and help navigate complex regulatory landscapes.

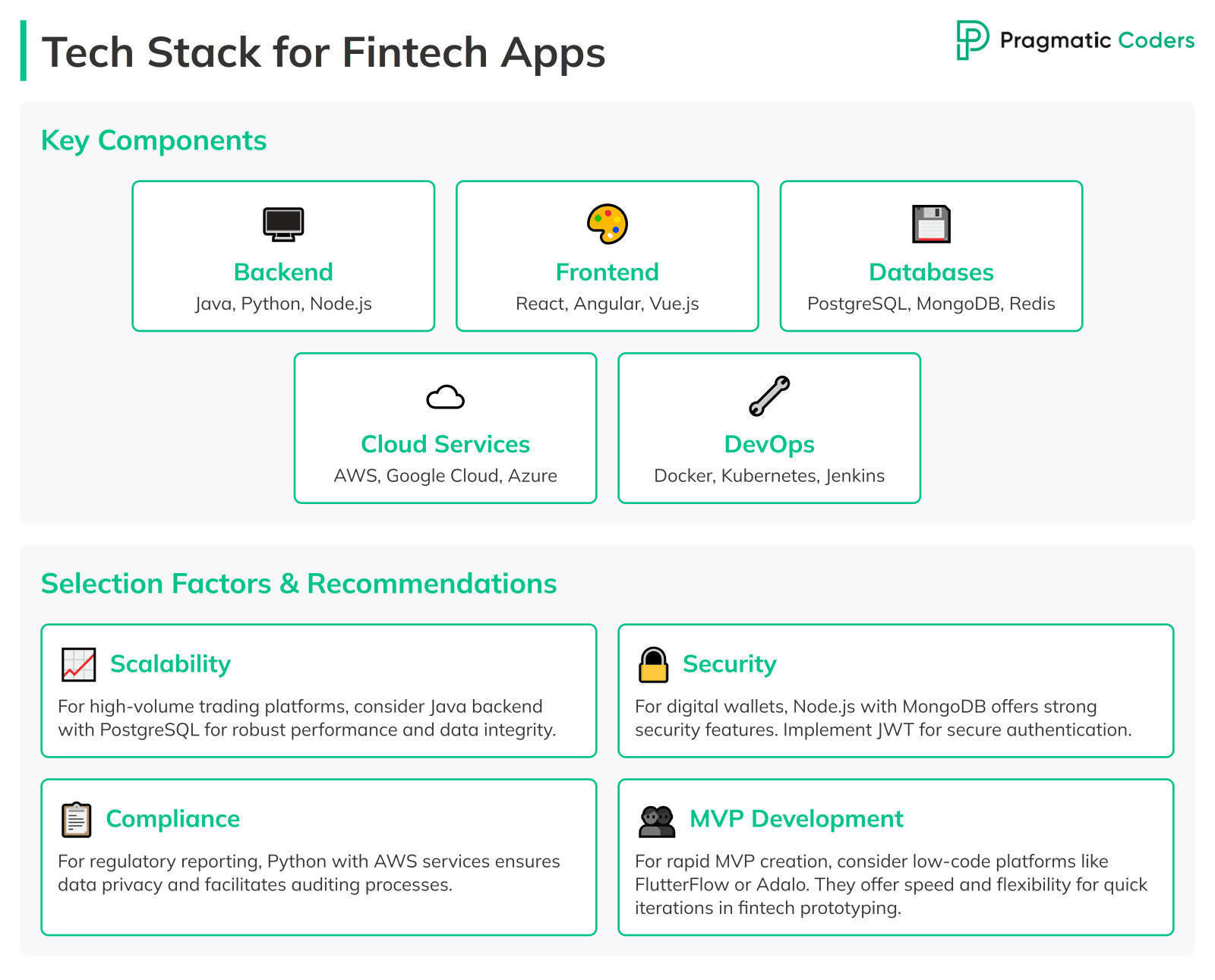

Technology Stack and Development

Choosing the right technology stack is crucial for building a scalable, secure, and efficient fintech platform.

Selecting the Right Tech Stack for Your Fintech App

Your tech stack should align with your product’s needs and your team’s expertise. Common components in fintech stacks include:

- Backend: Java, Python, or Node.js

- Frontend: React, Angular, or Vue.js

- Databases: PostgreSQL, MongoDB, or Redis

- Cloud Services: AWS, Google Cloud, or Azure

- DevOps: Docker, Kubernetes, Jenkins

Consider factors like scalability, security, and compliance when making your choices.

Balancing Innovation with Security and Scalability

In fintech, security and scalability are as important as innovation:

- Implement end-to-end encryption for all data transmissions

- Use multi-factor authentication for user accounts

- Regularly perform security audits and penetration testing

- Integrate banking APIs to streamline integration with financial institutions

- Design your architecture to handle rapid growth in users and transactions

- Use microservices architecture for easier scaling and maintenance

Implementing AI and Machine Learning in Fintech

AI and ML can significantly enhance your fintech product. Developing your own AI-based solutions might not be feasible due to limited funds or experience. Instead, leverage commodities and ready-made solutions. Key areas where AI can make a difference include:

- Fraud detection: Use ML algorithms to identify suspicious transactions.

- Credit scoring: Develop more accurate risk assessment models.

- Personalized financial advice: Offer AI-driven insights based on user behavior.

- Chatbots: Provide 24/7 customer support with AI-powered assistants.

- Predictive analytics: Forecast market trends or user behavior.

When implementing AI, ensure you have the right data infrastructure and comply with relevant regulations. This guide to building AI software is a must-read if you’re considering AI for your fintech solution.

The Role of Blockchain and Cryptocurrencies

These two have as many fans as they have doubters. Consider how blockchain and cryptocurrencies might fit into your fintech solution:

- Smart contracts for automated, trustless transactions

- Decentralized finance (DeFi) applications

- Cryptocurrency wallets or exchanges

- Blockchain for secure, transparent record-keeping

- Tokenization of assets

While blockchain offers exciting “get rich quick” possibilities, carefully evaluate its necessity for your specific use case. Not every fintech solution benefits from blockchain technology.

Fintech Product Development Best Practices

Follow these best practices throughout your development process:

- Adopt an Agile methodology for flexibility and rapid iteration

- Implement continuous integration and continuous deployment (CI/CD)

- Write clean, well-documented code for easier maintenance

- Conduct thorough testing, including unit tests, integration tests, and user acceptance testing

- Plan for scalability from the start, even if you’re starting small

Remember, in fintech, a solid product development strategy is a must. Invest time and resources in building a robust, secure, and scalable platform from the outset.

Regulatory Compliance and Risk Management

In the fast-paced world of fintech, regulatory compliance isn’t just a box to tick—it’s the foundation upon which you’ll build your entire business. As a fintech founder, you’ll need to navigate a complex web of regulations that can vary significantly depending on your specific niche and target markets.

Navigating Fintech-Specific Regulations

One of the first steps in your compliance journey should be identifying the regulations relevant to your business. For instance:

- In Europe: Familiarize yourself with the Payment Services Directive 2 (PSD2), which aims to make electronic payments more secure and foster innovation in the payment sector.

- In the United States: The Dodd-Frank Act will likely play a significant role in shaping your compliance strategy.

Many jurisdictions now offer “regulatory sandboxes” for fintech startups, providing a controlled environment where you can test your product under regulatory guidance. The UK’s Financial Conduct Authority (FCA) Sandbox, for example, has been instrumental in helping numerous fintech startups navigate the regulatory waters while fostering innovation.

Implementing Robust KYC and AML Processes

When it comes to Know Your Customer (KYC) and Anti-Money Laundering (AML) processes, a risk-based approach is key. Consider implementing a tiered KYC process based on the risk level of your customers:

- Low-risk customers: Basic identity verification might suffice

- High-risk individuals: Enhanced due diligence, including checks on their source of funds

Technology can be your ally in this endeavor. Artificial Intelligence and machine learning are revolutionizing KYC and AML processes, making them more efficient and effective. Companies like Onfido and Jumio offer AI-powered identity verification tools that can significantly streamline your onboarding process while ensuring compliance.

Data Privacy and Security Best Practices

Data privacy and security should be at the forefront of your mind from day one. Implement a comprehensive data protection strategy that includes:

- End-to-end encryption

- Strong access controls

- Regular security audits

Depending on your target markets, you’ll need to comply with regulations like GDPR in Europe or CCPA in California. Consider appointing a Data Protection Officer early on—even if it’s not legally required, it demonstrates your commitment to data privacy and can help build trust with your customers (don’t forget to leverage this in your marketing either!).

Building Relationships with Regulatory Bodies

Don’t wait for regulators to come to you. Be proactive in building relationships with regulatory bodies:

- Reach out to them early

- Share your plans

- Demonstrate your commitment to compliance

Joining industry associations like the Electronic Transactions Association can provide valuable resources and help you stay informed about regulatory developments.

Funding Your Fintech Business

Securing adequate funding is often one of the biggest challenges for fintech startups. As you embark on your funding journey, you’ll face a crucial decision: should you bootstrap or seek external funding?

Bootstrap vs. External Funding: Pros and Cons

Bootstrapping:

- Pros: Maintain full control, forces lean operations

- Cons: Limited resources can slow growth, challenging to compete with well-funded rivals

External funding:

- Pros: Access to larger capital pool for rapid growth, brings in expertise and networks of investors

- Cons: Dilution of ownership, pressure to deliver returns to investors

Attracting Venture Capital in the Fintech Space

If you decide to pursue venture capital, remember that in the fintech space, traction is key. VCs will be looking for:

- Clear evidence of product-market fit

- Metrics like user acquisition cost, customer lifetime value, and monthly recurring revenue

- Understanding of the regulatory landscape and strategy for compliance

Alternative Funding Options

Don’t overlook alternative funding options:

- Crowdfunding platforms like SeedInvest or Republic (specialize in fintech startups)

- Strategic partnerships with established financial institutions

- Accelerators and incubators (e.g., Y Combinator, Barclays Accelerator)

- For blockchain-focused fintechs: Initial Coin Offerings (ICOs) or Security Token Offerings (STOs)

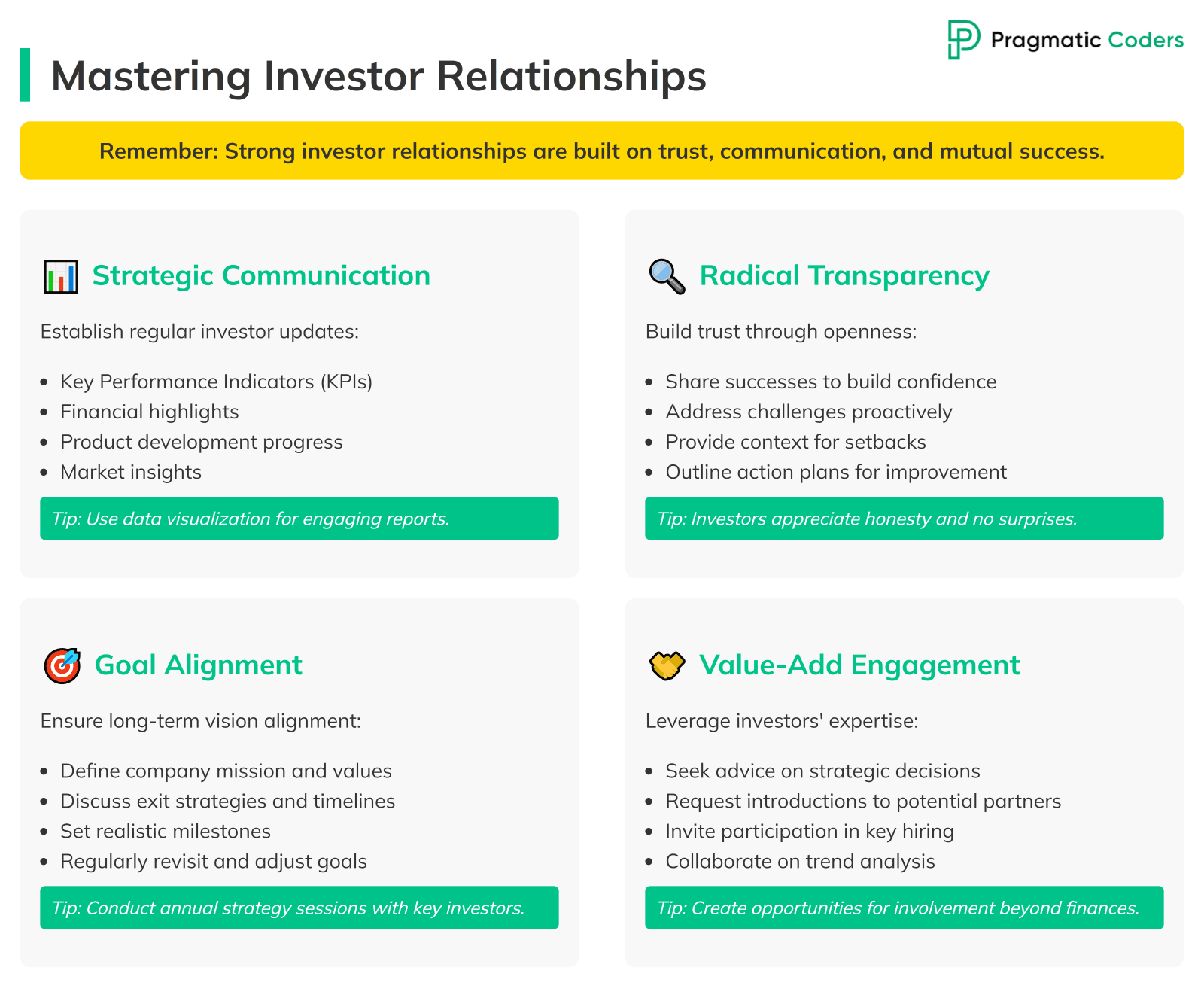

Managing Investor Relationships and Expectations

Once you’ve secured funding, managing investor relationships becomes crucial:

- Set up a regular cadence of investor updates

- Be transparent about challenges as well as successes

- Ensure alignment on long-term goals from the start

Remember, your investors can be valuable partners in your journey—don’t hesitate to leverage their expertise and connections.

Go-to-Market Strategy

Launching your fintech product is just the beginning of your journey. A well-crafted go-to-market strategy can make the difference between a product that gains traction and one that fades into obscurity.

Crafting a Compelling Brand Story

In the crowded fintech space, your brand story can set you apart. It’s not just about what your product does, but why it exists and who it serves. For example, Robinhood’s mission to “democratize finance for all” resonated strongly with millennials and Gen Z.

Your brand story should:

- Reflect your company’s values and mission

- Address how you’re making financial services more accessible or transparent

- Be authentic and consistently communicated across all touchpoints

Building Trust in The Fintech Sector

Trust is the currency of the financial world, and as a newcomer, you’ll need to earn it:

- Be transparent about your fees and how you make money

- Clearly communicate how you protect user data

- Consider publishing regular security audits or obtaining certifications

- Provide educational resources to help users understand financial concepts

For instance, Acorns offers a wealth of educational content alongside its investment products, helping users become more financially literate while using the app.

Leveraging Partnerships for Growth

Strategic partnerships can accelerate your growth by providing:

- Access to established customer bases

- Complementary technologies

- Regulatory expertise

Look for partners whose offerings complement yours. For example:

- A personal finance app could partner with a credit score provider

- A lending platform could partner with a credit bureau to enhance underwriting capabilities

Scaling Strategies for Fintech Startups

Scaling a fintech startup presents unique challenges. Here are a few strategies to consider:

- Modular Architecture: Build your tech stack to easily add new features or scale existing ones without disrupting the entire system.

- Regulatory Scalability: Ensure your compliance processes can handle increased volume and expand to new jurisdictions as you grow.

- Customer Service Scalability: Consider AI-powered chatbots and self-service options to handle common queries as your user base grows.

- Data Scalability: Ensure your data infrastructure can handle growing volumes of data while maintaining performance and compliance with data protection regulations.

- Cloud Solutions: Leverage cloud solutions to quickly scale resources up or down based on demand, ensuring cost efficiency and flexibility. Learn more from our guide to cloud computing in banking.

Remember, scaling isn’t just about growing your user base—it’s about growing sustainably while maintaining the quality of your product and service.

Measuring Success and Iterating

In the fast-paced world of fintech, the ability to measure your performance and quickly iterate on your product is crucial for long-term success.

Key Performance Indicators for Fintech Startups

While specific KPIs depend on your particular fintech niche, here are some universal metrics to consider:

- Customer Acquisition Cost (CAC)

- Customer Lifetime Value (CLV)

- Monthly Active Users (MAU)

- Churn Rate

- Transaction Volume and Value

For specific types of fintech products:

- Lending platforms: Default rates, average loan size

- Investment apps: Assets under management (AUM), average return on investment

Gathering and Acting on User Feedback

Implement multiple channels for gathering feedback:

- In-app feedback tools

- Regular user surveys

- User testing sessions

- Social media monitoring

- Customer support interactions

Establish a process for reviewing and prioritizing user feedback. Consider using a framework like the Kano model to categorize features based on their potential impact on user satisfaction.

Pivoting Strategies When Necessary

Sometimes, despite your best efforts, your initial product doesn’t resonate with the market as expected. Signs that it might be time to pivot include:

- Low user engagement or high churn rates

- Difficulty acquiring customers at a sustainable cost

- Regulatory hurdles that make your current model unviable

- A significant market shift that impacts your value proposition

If you decide to pivot, communicate clearly with your team and investors. Explain the rationale behind the decision and outline your new direction.

Planning for Long-term Sustainability

While early startup days often focus on growth at all costs, keep an eye on long-term sustainability:

- Focus on retaining users and turning them into profitable customers

- Consider diversifying your revenue streams as you grow

- Stay agile and be prepared to evolve your product and business model as the market changes

Remember, building a successful fintech startup is a marathon, not a sprint. By consistently measuring your performance, listening to your users, and being willing to adapt, you’ll be well-positioned for long-term success in this exciting and dynamic industry.

Case Studies: Successful Fintech Startups

Understanding the journeys of successful fintech startups can provide invaluable insights for aspiring entrepreneurs. Let’s examine two recent success stories and extract key lessons.

Stripe: Simplifying Online Payments

Stripe, founded by Irish brothers Patrick and John Collison in 2010, has revolutionized online payments. What started as a simple idea to make it easier for businesses to accept payments online has grown into a company valued at $95 billion as of 2021.

Key success factors:

- Focusing on developers: Stripe made its API incredibly easy for developers to integrate, reducing implementation time from weeks to minutes.

- Constant innovation: Stripe consistently expanded its product offerings, from basic payments to fraud prevention, billing, and even corporate cards.

- Global expansion: The company methodically entered new markets, adapting to local payment methods and regulations.

Lesson learned: Stripe’s success demonstrates the power of solving a specific pain point exceptionally well, then expanding strategically based on customer needs and market opportunities.

Robinhood: Democratizing Investing

Robinhood, founded in 2013 by Vladimir Tenev and Baiju Bhatt, aimed to make investing accessible to everyone, particularly millennials. Despite recent controversies, the company’s impact on the investment landscape is undeniable.

Key success factors:

- User-friendly design: Robinhood’s app made investing feel like a game, appealing to younger users.

- Commission-free trades: This revolutionary model forced established brokers to follow suit.

- Educational content: Robinhood provided resources to help novice investors understand the market.

Lesson learned: Robinhood’s story highlights the potential of targeting underserved segments with a user-friendly product. However, it also serves as a cautionary tale about the importance of robust risk management and clear communication, especially in highly regulated industries.

These case studies underscore that success in fintech often comes from:

- Identifying a clear market need

- Leveraging technology to address it in a user-friendly way

- Being prepared to evolve rapidly in response to market dynamics and regulatory changes

Conclusion

Starting a fintech company is not for the faint of heart. The road ahead will be challenging, filled with regulatory hurdles, fierce competition, and the constant need to innovate. However, for those willing to persevere, the rewards can be substantial – both financially and in terms of making a real impact on how people interact with money and financial services.

Remember:

- Some of today’s most successful fintech companies started with a simple idea and a commitment to solving a specific problem.

- Stay curious, remain adaptable, and never lose sight of the problem you’re trying to solve.

- The fintech industry is ripe with opportunities for those bold enough to seize them.

With careful planning, relentless execution, and a bit of luck, your fintech startup could be the next success story worth writing about.